Syria Special Report: Repeal of Caesar Act expected to accelerate business re-entry into Syria in 2026; major structural, security challenges to persist

Authors:

This report was written by:

- Ishika Garg – Intelligence Manager, MENA Division

- Matteo Sbarigia – Intelligence Manager, MENA Division

And reviewed by:

- Kez Gould – Associate Director, MENA Division

Executive Summary:

- International sanctions relief throughout 2025, culminating in the repeal of the Caesar Act, underscored Western confidence in the new Syrian government and substantially reduced the legal and compliance barriers that had precluded international engagement with the country.

- This is expected to enable a gradual increase in investment and commercial activity, although multiple structural and security risks will continue to challenge a return to operations in Syria.

- Extensive infrastructure damage, persistent electricity shortages, and underdeveloped banking channels will contribute to elevated logistics and operating costs, constraining the pace and scale of foreign companies’ re-entry.

- Despite a relative stabilization of the security environment, the risk of armed conflict, militancy, and sectarian violence will compound threats to personnel and assets.

- Overall, this will necessitate adherence to safety precautions and extensive contingency planning to initiate and sustain operations, despite the emerging range of business opportunities in the country.

Introduction:

Since the ousting of Bashar al-Assad in December 2024, the President Ahmad al-Sharaa-led government has rapidly reconfigured its foreign relations, governance structures, and economic orientation. Early outreach by Turkey and Qatar, including the reopening of diplomatic missions and the provision of energy and logistical support, was followed by participation from major regional powers, including Saudi Arabia and the UAE. Western governments adopted a more cautious approach, initially conditioning deeper engagement on security cooperation, protection of minorities, and a demonstrable shift from the former government’s authoritarianism toward inclusive governance. Despite some setbacks, President al-Sharaa formed a transitional government and reached several major milestones. This included integrating many non-armed groups into the Ministry of Defense and holding parliamentary elections in October 2025. These measures have been deemed sufficient by the West to create conditions for expanded international involvement in Syria after more than a decade of isolation. This has resulted in notable, high-level diplomatic engagement, including Syrian state visits to Washington, delegations of foreign officials visiting Damascus, and the easing of the wide-ranging, crippling sanctions regime imposed on Syria under al-Assad.

Assessments & Forecast:

Repeal of Caesar Act marks milestone in sanctions relief

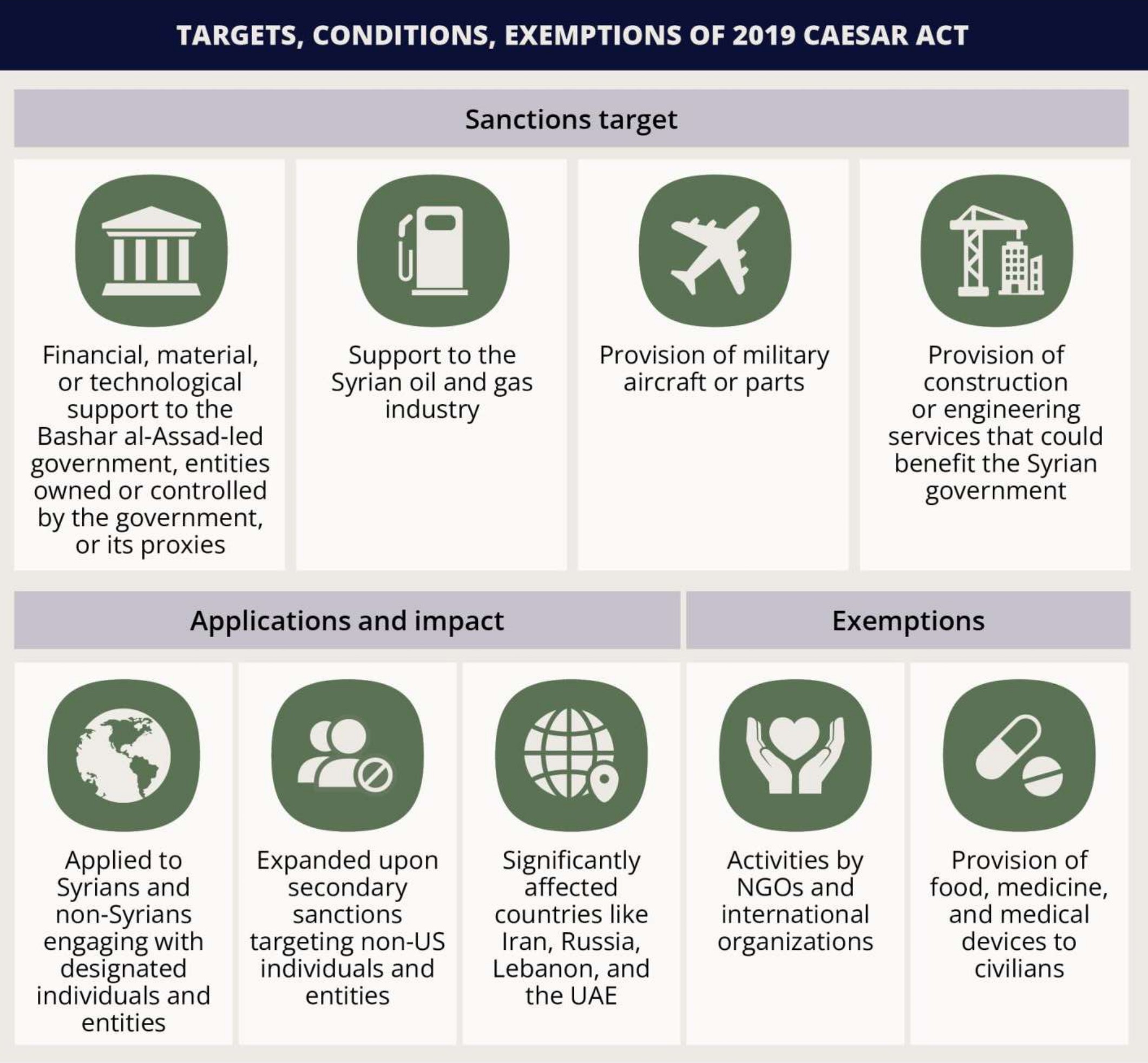

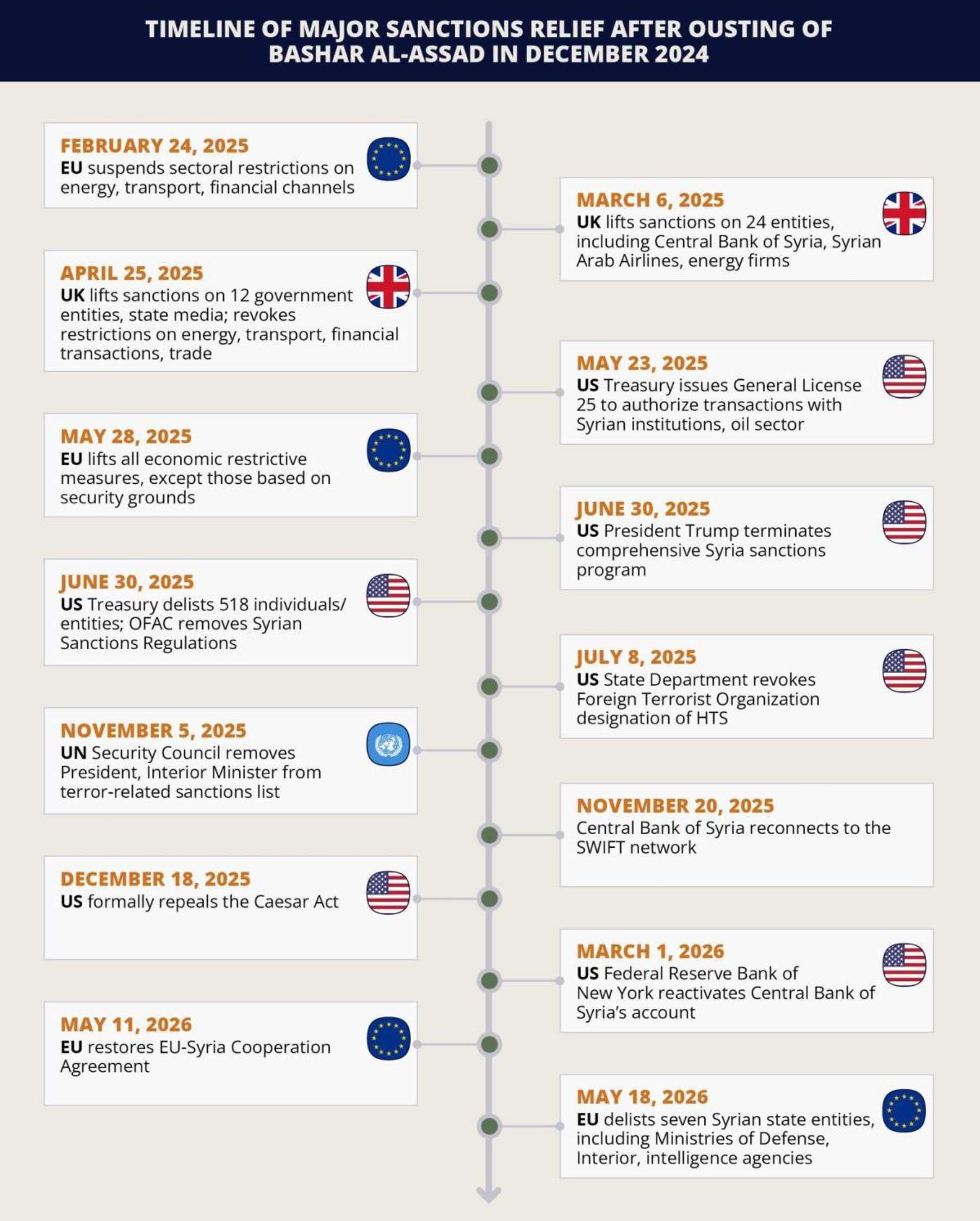

- The gradual dismantling of the extensive sanctions architecture throughout 2025, including the issuance of temporary waivers by the US and the removal of punitive measures against certain sectors, culminated in the milestone repeal of the 2019 Caesar Syria Civilian Protection Act (Caesar Act) in December 2025.

- The Caesar Act sanctions were among the most stringent measures imposed on Syria under al-Assad. The provisions extended secondary sanctions to non-US actors who engaged in construction, energy, and financial dealings with Syrian state entities. This became the primary deterrent constraining international engagement or investment in Syria, with its secondary-sanctions design carrying significant legal and reputational exposure risks, triggering a risk-averse approach among foreign firms even where activity was technically permissible.

- Decisions taken by President Trump’s administration throughout 2025 reflect its assessment that the sanctions in place at that time would significantly constrain the new government’s ability to initiate Syria’s socioeconomic recovery. This is underscored by the decision to issue General License (GL) 25 in May 2025, which marked another milestone providing immediate sanctions relief for a broad range of activities.

- Similarly, the US Treasury’s Office of Foreign Assets Control (OFAC) removed the Syrian Sanctions Regulations and delisted most Syrian entities after an Executive Order (EO) signed in June 2025, effectively terminating the old Syria sanctions program. This, along with the US Department of Commerce’s easing of export licensing requirements for civilian goods and software in August 2025, provided the most significant legal basis for updating corporate compliance frameworks and facilitated the re-entry of civilian technology and service providers into the Syrian market. This was evidenced by the return of several multinational technology company operations, including Google, Apple, Samsung, and Meta, between August and October 2025.

- The permanent repeal of the Caesar Act was, however, the most consequential step because it removed the remaining source of uncertainty surrounding the durability of sanctions relief up until this point. While the Trump administration’s 180-day waivers in May and November 2025 had already eased restrictions in practice, the temporary nature of these measures sustained investor caution driven by the short renewal cycle and the persistent risk of reversals, which are of particular importance for longer-term contracts and engagement.

- In addition to the permanent nature of the move, the legislative repeal in the National Defense Authorization Act for Fiscal Year 2026 eliminated the legal basis for the automatic reimposition of sanctions after each waiver expired. This was replaced with a review mechanism focused on periodic White House reports to Congress on the Syrian government’s counter-Islamic State (IS) efforts, protection of minorities, and the role of foreign fighters within state institutions. In turn, this now renders sanctions enforcement solely subject to political oversight, diluting mandatory compliance requirements for the Syrian government to non-binding commitments it should aspire to meet.

- FORECAST: A broad reimposition of sanctions on Syria is therefore highly unlikely, although targeted restrictions on specific individuals and entities remain in place. Gulf countries also actively advocated for sanctions relief, entrenching their political and financial interests in Syria’s recovery efforts. This will provide an additional layer of stakeholders interested in preventing a renewed economic isolation of Syria by the West.

- FORECAST: Overall, this will reduce the compliance risks associated with operating in Syria, which will likely prompt an increase in entities seeking to re-enter the country for business in 2026. This report will examine the continued logistical challenges and security risks associated with operating in Syria.

Infrastructural challenges:

- Infrastructure in Syria has been severely degraded by over a decade of civil war and sanctions-driven restrictions on recovery. The World Bank has estimated total damage to physical, social, and other infrastructure at approximately 8.7-11.3 billion USD. Transport networks, electricity generation and distribution, and water and sanitation systems were among the most heavily affected sectors, pointing to the scale of damaged infrastructure that the new authorities must rehabilitate.

- In this context, Syrian authorities have increasingly sought to formalize reconstruction opportunities for private investors. This is evidenced by the Syrian Investment Authority’s (SIA) publication of hundreds of projects across the infrastructure, logistics, tourism, and services sectors.

- Many are structured as Build-Own-Operate (BOO), Build-Transfer-Operate (BTO), or broader Public-Private Partnership (PPP)-style arrangements, reflecting Damascus’ efforts to attract foreign private capital. This is likely due to the state’s limited fiscal capacity and the scale of reconstruction needs. However, the viability and timelines of such projects will continue to be hindered by implementation challenges, including infrastructure-related issues discussed below, which will pose a significant hurdle for businesses looking to enter Syria.

Transportation

Air travel

- Since the Hay’at Tahrir al-Sham (HTS)-led takeover, international connectivity has improved more rapidly than domestic networks. Damascus International Airport (DAM) reopened to international traffic in January 2025, followed by Aleppo International Airport (ALP) in March 2025, underscoring the prioritization of Syrian authorities to restore international access and logistical connectivity, which will likely be critical for Syria’s broader socioeconomic recovery.

- However, passenger and cargo flow reportedly continues to rely heavily on outdated digital infrastructure, including in air traffic control centers. Airports also reportedly lack appropriate radar equipment, while significant concerns persist over the authorities’ ability to meet international aviation standards. The need to upgrade Syria’s airport infrastructure is pertinently demonstrated by major deals signed in recent months to modernize state facilities. This includes a four billion USD deal to upgrade DAM signed in November 2025 with a Qatar-led consortium, in addition to a major deal signed with Saudi Arabia on February 7 entailing the establishment of a joint Syrian airline, the redevelopment of ALP, and the construction of a new airport in Aleppo.

- FORECAST: While these major strategic projects will significantly improve Syria’s international connectivity in the long term, short-term challenges will persist, hindering the country’s ability to absorb a considerable uptick in air traffic. This will continue to impact businesses on the ground in 2026, particularly for time-sensitive logistics.

Land travel

- Overland connectivity has slowly improved since December 2024. This has been partly facilitated by Syria’s reintegration into regional transport networks, as evidenced by the June 2025 MoU between Ankara and Damascus abolishing transshipment requirements at border crossings. While such deals will ease administrative constraints on direct road transport and freight movement on key corridors linking Syria with Turkey, Jordan, and the Gulf, considerable challenges will remain to domestic road travel.

- Degraded road conditions and inconsistent maintenance will keep transit times and accident risks elevated, particularly for movements on more minor roads and outside major urban centers. Prominent thoroughfares will also require extensive rehabilitation. This includes the M4 highway, connecting Aleppo to Raqqa and the northeast, which was impacted by the territorial fragmentation between the Syrian Democratic Forces (SDF) and the central government, preventing restoration work along a logistics corridor.

- Travel within Syria will be further constrained by the continued paralysis of large segments of Syria’s rail network. The Syrian Transport Minister reportedly stated that only 1,052km of rail networks are functioning out of 2,800km available, with repairs estimated to cost around 5.5 billion USD, which would take between three and five years to complete.

- FORECAST: This will further constrain logistics for businesses seeking to operate in the country, which may impede the internal transfer of materials, particularly in the construction sector. However, significant investments are likely in the long term, with reported tripartite discussions to establish a transnational railway from Turkey to Saudi Arabia through Syria and Jordan.

Sea travel

- Maritime connectivity demonstrated clear signs of recovery in 2025. A maritime data company reported a 769 percent surge in seaborne trade in December 2025 compared to December 2024. This underscores that Syria’s ports of Tartus, Latakia, and Baniyas are already capable of supporting basic commercial operations and accommodating higher vessel arrivals and cargo volumes.

- This trend is likely to accelerate in 2026, with foreign firms expected to explore investments in Syria’s maritime infrastructure given its strategic location on the Mediterranean Sea. This is already demonstrated by major deals signed last year, including the May 2025 agreements with France’s CMA CGM for the Latakia Port and the UAE’s DP World for the Tartus Port, highlighting the willingness of foreign operators to pursue long-term deals in Syria within the emerging post-sanctions framework.

- FORECAST: That said, such agreements and projects will take several years to implement and complete. Outdated handling equipment, limited channel depth for larger vessels, and the absence of fully integrated port systems will continue to limit port capacity and efficiency in the short term at least. Syria’s ports will therefore likely remain vulnerable to handling surges in demand, adverse weather conditions, and potential congestion, which could mean prolonged vessel waiting times, unreliability of schedules, supply chain disruptions, and higher logistics costs.

Energy

- Energy availability remains one of the most immediate constraints on economic stabilization and the re-entry of businesses in the country due to Syria’s degraded generation capacity and transmission infrastructure through many years of civil war and fragmented territorial control.

- Prior to the civil war, Syria was estimated to have around 8,500 MW of installed power capacity. However, in February 2025, the Energy Ministry indicated that this had fallen to 1,300 MW, likely due to damage to power plants, transmission lines, and distribution networks, and a lack of fuel preventing plants from operating at full capacity.

- Despite some improvements over the past year, particularly in major cities such as Damascus, where electricity coverage appears to have steadily increased, challenges will likely remain. Syria is estimated to require approximately 6,500 MW to provide 24-hour electricity coverage. This will require years of sustained investment and major repairs to the grid.

- Another critical factor will be re-establishing a reliable fuel supply. Several agreements with foreign countries over the past year underscore that Syria is not self-sufficient in this regard. This is despite extensive oil and gas reserves that are primarily located in the northeastern region, which formerly fell under Kurdish, rather than government, control. In this context, energy flows from this area were previously subjected to disruptions due to the state of armed conflict in recent years. This is both in terms of physical distribution, which was impeded by damaged infrastructure, and the lack of cooperation between the state and Kurdish forces overseeing output and distribution from this region.

- However, the January 30 comprehensive agreement between the Syrian government and the SDF formalized the integration of territory and energy resources previously held by the Kurdish forces under state control. This will enable the resumption of crude oil and gas transfers toward refineries in western Syria, improving fuel supply and energy generation. It will complement energy supply agreements signed with foreign partners over the last year. These included a March 2025 arrangement to supply LNG from Qatar via Jordan to the Deir Ali plant, south of Damascus, and the supply of Azerbaijani gas via Turkey to Aleppo through Qatari funding since August 2025.

- Additionally, major energy disruptions resulting from the US/Israel and Iran war have elevated Syria’s strategic relevance as an energy and transit corridor. On April 16, Iraq announced the commencement of crude loading operations through Syria’s Baniyas terminal for export to European markets under a transit-and-re-export arrangement, with Syria retaining a portion of the crude to support domestic power generation. This was followed by Iraq’s May 1 announcement that oil exports to Syria through the recently reopened Rabia border crossing had formally resumed. These developments underscore Syria’s strategic geographical positioning linking Iraq, the Gulf, and the Mediterranean Sea, which Damascus will continue to leverage to attract foreign investment in the sector. This is particularly amid ongoing uncertainty over the viability of oil and gas exports via the Persian Gulf, which partly undermines enthusiasm for the India-Middle East-Europe Economic Corridor (IMEC), which was a key scheme promoted by Washington during former President Joe Biden’s term.

- FORECAST: In 2026, energy availability is therefore expected to improve incrementally, particularly in urban and industrial zones. However, electricity shortages resulting in regular and potentially widespread outages will persist in the coming months, particularly in outlying areas outside major cities. This will constrain operations, logistics, and energy-intensive activities, with companies required to utilize private generators and integrate unplanned outages into their costs.

Banking and financial sectors

- Another major consideration for businesses looking to re-enter Syria for operations in 2026 will be the financial landscape. Banking, insurance, and trade finance adjusted more slowly to the gradual lifting of sanctions in 2025. The reconnection of international payment networks, namely Visa and Mastercard, to Syrian domestic banks on May 4 already constitutes a critical step toward facilitating e-commerce, reducing reliance on cash transactions and informal channels, and gradually improving payment processing capabilities for businesses operating in Syria.

- However, correspondent banking relationships (CBRs) and cross-border financial channels, which had been previously severed, only began to be re-established in 2025. This was supported by the easing of restrictions on Syrian financial institutions by Western countries in 2025 and 2026, including measures permitting correspondent engagement with the Commercial Bank of Syria. However, the slow progress has constrained access to trade finance, letters of credit, and cross-border settlement, reflecting the cumulative effect of prior compliance with sanctions and heightened Anti-Money Laundering and Counter-Terrorism Financing (AML/CFT) requirements. Syria’s continued grey-listing by the Financial Action Task Force (FATF) compounded this by increasing due diligence requirements and scrutiny by international banks, even in the absence of explicit prohibitions.

- The Central Bank of Syria’s (CBS) reconnection to the SWIFT international payments system in November 2025 marked a milestone, restoring Syria’s ability to process trade-related payments, route remittances through formal channels, and improve transparency for international trade and foreign investment. However, its impact remains contingent on partner banks’ likely limited willingness to establish or expand CBRs. This is particularly given that Syria continues to be designated as a State Sponsor of Terrorism (SST) by the US State Department, sustaining elevated reputational risks. This will continue to discourage large Western banks, insurers, and investors from funding projects or backing businesses operating in Syria.

- FORECAST: Overall, this highlights that firms and businesses seeking to engage in Syria in 2026 will continue to face challenges, despite increasing access to banking and financing in the country. Financial flows will likely require routing through a limited number of regional banks, which, together with the substantial difficulties in establishing CBRs, will increase processing times and transaction costs. While the SST designation, based on the trajectory of US actions in 2025, is likely to be rescinded in the coming months, it will continue to constrain access to credit in the short term at least. Combined, these factors will elevate costs for businesses.

Security challenges:

In addition to economic hurdles, there are a range of security issues that will challenge business re-entry into Syria. While the overall security environment has stabilized, it remains fragmented and volatile in different areas. The key drivers of instability include the risk of armed conflict, militancy, and sectarian tensions.

Armed Conflict

Since the December 2024 takeover, the government has focused on the integration and gradual monopolization of armed groups and territorial control in Syria. Despite relatively broad success in both endeavors, including the integration of most non-state actors into the Ministry of Defense in January 2025 and the establishment of government control across most territory, several outlying challenges persist. These unresolved issues continue to generate localized clashes, which at times escalate into broader waves of armed confrontations.

Kurdish forces in northeastern Syria

- Despite the March 2025 agreement for the Kurdish Syrian Democratic Forces (SDF) and Autonomous Administration of North and East Syria (AANES) to integrate into state structures, this process became stagnated and resulted in eruptions of largely localized armed clashes throughout the year in northeastern Syria. This was primarily due to Kurdish resistance to integrate over concerns regarding the conduct of the Islamist government forces against the Kurdish population and its desire to retain some autonomy.

- The failure to implement the framework resulted in a major eruption of armed conflict in January, following the government’s decision to launch rapid offensives to oust Kurdish forces in Aleppo city, the wider province, and eventually vast swathes of northeastern Syria that were under AANES control. The success of the government campaign, which significantly increased Damascus’ leverage, in addition to pressure from international stakeholders such as Turkey and the US, prompted the SDF and AANES to sign a comprehensive ceasefire deal on January 30.

- Under the framework, the government has begun to assume control of all territory, integrate former SDF brigades into the Syrian Arab Army (SAA), and grant Kurdish military figures largely symbolic positions. No major flare-ups of hostilities have materialized since, constituting a success for Damascus and leading to relative stabilization in the region.

- FORECAST: However, mistrust persists between the Islamist government and segments of the Kurdish forces/population, resulting in localized and sporadic instances of unrest during the government’s takeover in some areas. This risk will persist, with more likely hotspots being the Kurdish-majority cities of Kobani and Qamishli, where government forces will be deployed, and in the mixed al-Hasakah city, which was a major point of contention in the latest campaign.

- FORECAST: Moreover, despite initial success in the integration of some SDF units into the SAA and the deployment of these forces to potential friction points formerly held by the AANES, practical gaps remain. This includes the alignment and training of forces. Additionally, former SDF Commander and now Deputy Defense Minister of the Eastern Region Siban Hamo warned that the number of former SDF personnel exceeds the new brigades that have been formed. This increases the risk of disenfranchisement, which could lead sidelined former SDF fighters to join more hardline groups that refused to integrate with the SAA. Such militias could resort to attacking government positions.

- Concurrently, Damascus will face the challenge of controlling more radical armed factions that were integrated into its ranks shortly after the ousting of al-Assad, several of whom were suspected of perpetrating atrocities during previous bouts of sectarian clashes over the last year (see below). Such actors could also oppose the integration of former SDF personnel into the national military.

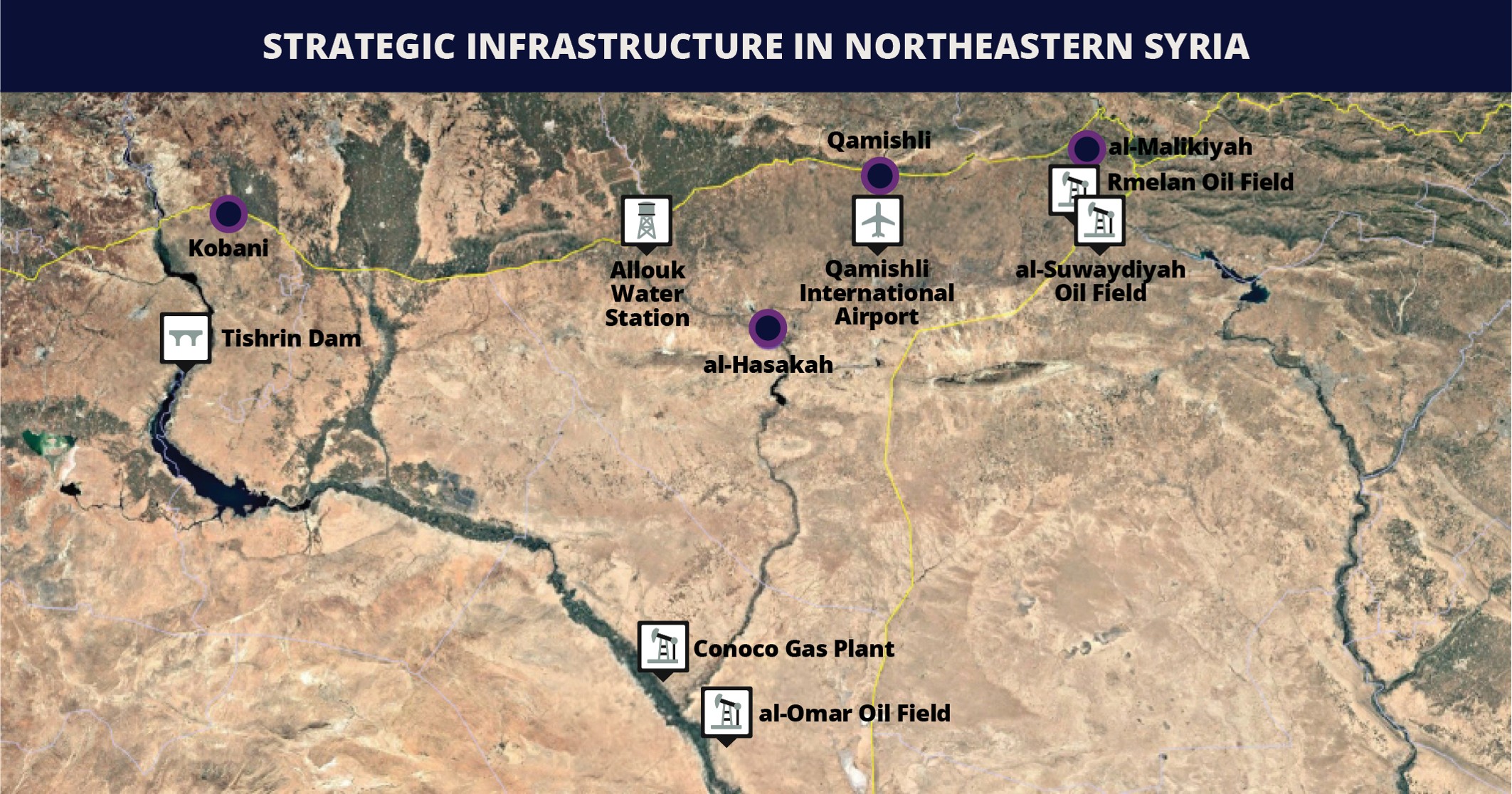

- FORECAST: Overall, this will sustain volatility in the region. This is an important consideration for both potential investors in Syria and the government, given the high concentration of strategic infrastructure in northeastern Syria, including energy assets, transportation hubs, and logistics infrastructure (see infographic below).

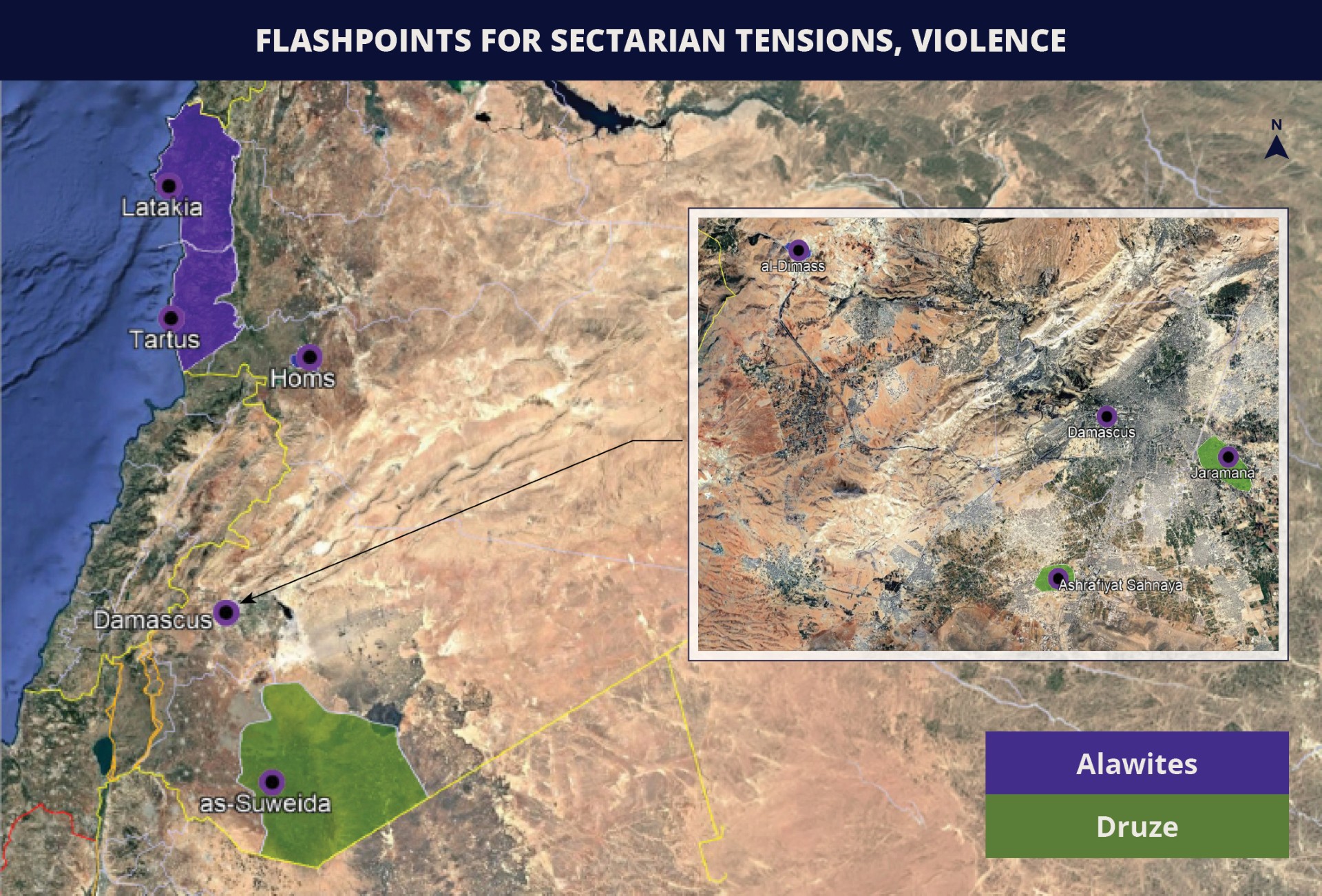

Druze forces in southern Syria’s as-Suweida

- Another major arena for armed conflict is southern Syria’s Druze-majority as-Suweida, which continues to be governed by Druze religious leadership. This includes Hikmat al-Hijri, who established the National Guard and strongly opposes the influence of the Islamist government, with which it has clashed on several occasions since December 2024.

- The most notable eruption occurred in July 2025, triggered by mutual kidnappings by Bedouin residents near as-Suweida and Druze militiamen. This prompted extensive violence, including clashes on major thoroughfares in the area such as Route 110, which also spread to Druze locales near Damascus such as Rif Dimashq’s Jaramana and Sahnaya.

- As underscored in this outbreak, sectarian violence specifically involving Syria’s Druze community is also a trigger for Israeli strikes, reflecting Jerusalem’s pledge to protect the sect from perceived extremists within the government. This has entailed Israeli warning strikes against the Syrian government’s military infrastructure in Damascus, in addition to periodic strikes against such assets in southern Syria.

- FORECAST: Following the government’s offensive against Kurdish forces in northeastern Syria, tensions and the Druze threat perception toward Damascus have likely increased. This is supported by al-Hijri’s calls for protests and a large-scale demonstration recorded in as-Suweida demanding Druze self-determination on January 31, in addition to sustained, localized clashes recorded since.

- FORECAST: This may suggest that some of the Druze leadership view the Syrian government’s offensive against Kurdish forces as preluding a similar operation against the Druze in as-Suweida. This is particularly given the organized opposition in the province, including politically through the “Supreme Legal Committee,” and militarily through the National Guard, which are both under the influence of Hikmat al-Hijri, who enjoys popular support. In this vein, the government likely views the Druze community as capable of offering more cohesive and sustained resistance to government forces and thus posing a threat to the government.

- FORECAST: While any potential plans for a broader government operation were likely delayed amid the regional war and evolving security priorities, the risk for such a scenario will be elevated over the coming months. As the final major area falling outside government control, as-Suweida will likely remain a sensitive and potentially volatile arena, with any renewed escalation carrying risks of collateral damage and operational disruptions.

al-Assad loyalists in northwestern Syria

- While relatively less organized than Druze and Kurdish militias, cells affiliated with former President Bashar al-Assad also pose a threat to the new government and undergird the risk of armed conflict in the country. These elements are primarily concentrated in former al-Assad strongholds, particularly in northwestern Alawite coastal areas such as the Latakia and Tartus provinces, where sporadic attacks have been recorded. For example, following the HTS-led takeover, al-Assad loyalists launched a series of attacks against government forces in January 2025, followed by a coordinated attack in the Jableh area in March 2025.

- Loyalist groups, such as the Coastal Shield Brigade, the Men of Light Brigade, and the Syrian Popular Resistance, appear largely fragmented. They likely comprise security personnel of the former regime, local militia members, and tribal networks with historical ties to the al-Assad establishment. There is no clear unified command structure or identifiable umbrella organization directing or coordinating operations. As a result, attacks by al-Assad loyalists have not followed a fixed pattern and have occurred sporadically. This trend is likely to continue.

- FORECAST: In the absence of a more organized and cohesive loyalist network, these actors are unlikely to pose a significant challenge to the authorities in terms of contesting territorial control. However, they are likely to continue launching asymmetric attacks to undermine the government. An uptick in attacks may trigger targeted security operations against localized cells, which could lead to armed clashes or surges of retaliatory violence that would increase the risk of collateral damage. This risk of cyclical violence will likely be elevated around events of national significance, such as Liberation Day, marking the overthrow of al-Assad’s government.

Outlook:

FORECAST: Overall, these threat vectors depict several higher-risk areas of the country for armed conflict: Kurdish-majority parts of northeastern Syria, southern Syria’s Druze-majority as-Suweida, and Alawite regions in the northwestern part of the country. This will continue to pose a major challenge given the significant threat of collateral damage to employees and assets, which will increase both risks and insurance costs, in addition to disruptions to operations associated with outbreaks of violence. These threats are expected to persist in the coming year as the government continues to consolidate its control over territory and outstanding armed groups.

Militancy

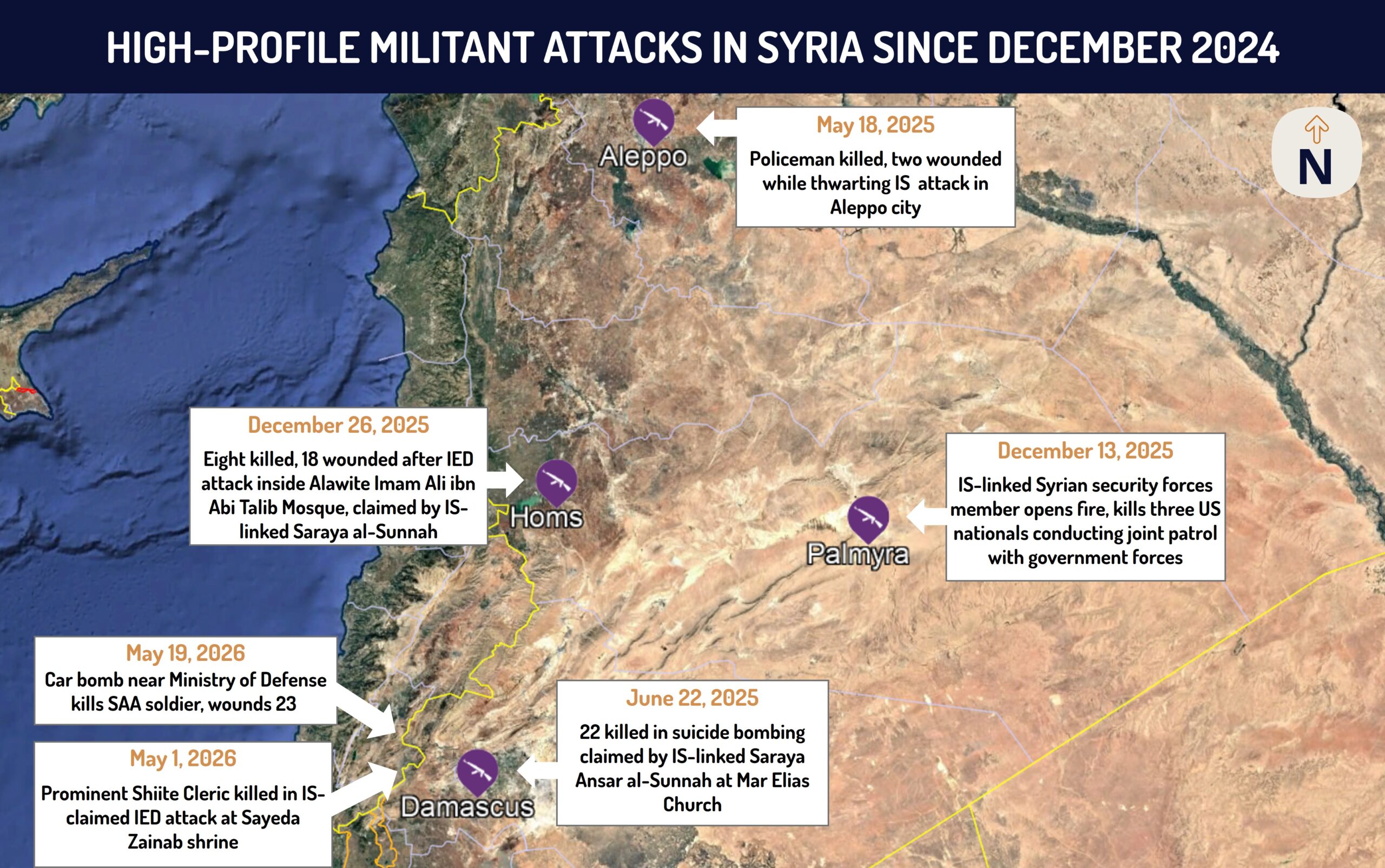

Militancy poses one of the most significant security risks to the government and business operations in the country. Since December 2024, Syria has witnessed several high-profile terrorist attacks (see infographic below). These have ranged from targeted attacks against minority institutions, state facilities, government forces, and on one occasion against US forces. The primary actors perpetuating this threat are jihadist groups and Iran-linked actors.

Jihadist actors

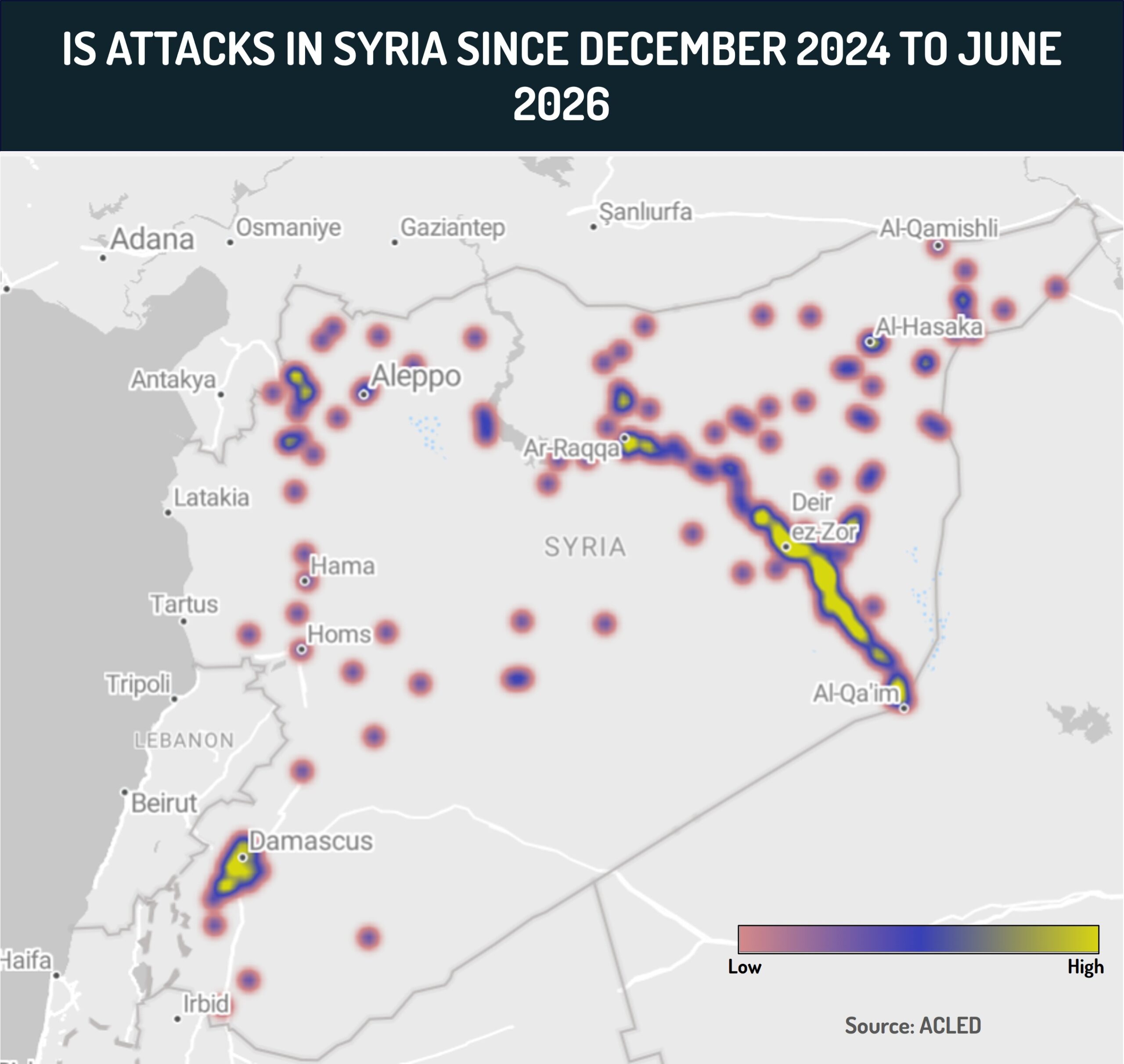

- Despite its broad decline in recent years, the security vacuum that emerged following al-Assad’s ousting and the presence of large, abandoned SAA weapons depots and warehouses enabled the Islamic State (IS) to access military-grade weapons. This has bolstered its operational capabilities, boosted the group’s morale, and led to an apparent uptick in IS attacks and concerns of a resurgence in the country.

- According to open-source data, the top three provinces affected by IS attacks are Deir Ezzor, al-Hasakah, and Raqqa (see heat map below), highlighting the significant terror threat in northeastern Syria, where many strategic assets such as oil and gas fields are located. This may be due to security gaps arising along former frontlines of territorial control between the government and AANES, particularly in Deir Ezzor and al-Hasakah, as underscored by recent IS-claimed attacks in these locales. Several such incidents have taken place near strategic transport routes, including the M5 highway, highlighting IS’s ability to threaten critical infrastructure and disrupt business operations across Syria.

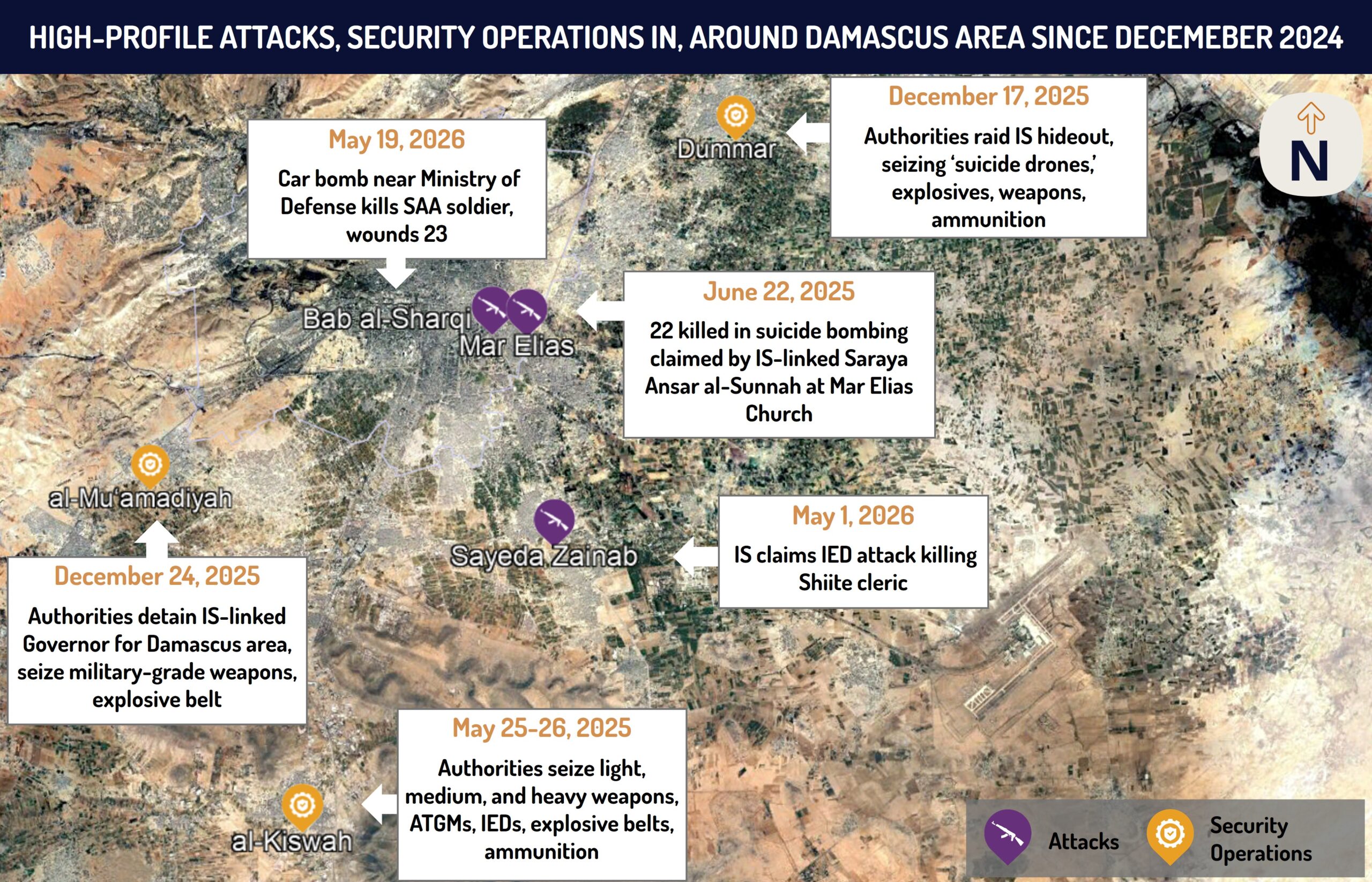

- Areas surrounding Damascus in Rif Dimashq province have emerged as another particularly notable flashpoint for such activity, as similarly depicted in the heatmap and the infographic below. Successful jihadist attacks, either by IS or the affiliated Saraya al-Sunnah, have also materialized in the capital, including a suicide bombing at the Mar Elias Church perpetrated by Saraya al-Sunnah in June 2025, and an IS-claimed IED attack targeting a Shiite cleric in Sayeda Zainab, located between DAM and Damascus, on May 1.

- Additionally, this region has recorded one of the highest numbers of counter-militancy operations (eight) since Syria’s admission to the US-led Coalition to Defeat IS in November 2025. Authorities have seized military-grade arms and high-ranking IS members in outlying areas near the capital, pointing to a significant threat of militancy near Damascus, which likely remains a key target for the group. This is particularly in light of the anticipated influx of business operations, which are likely to have some presence in the capital or at least pass through it, given its status as a major transport hub in the country.

- The gravity of the IS threat is further underscored by the extent to which Western engagement with Syria has focused on countering the group’s resurgence. This has become a focal point of cooperation, with the US, UK, and France conducting airstrikes on IS sites in recent months, while Washington has also shared intelligence of imminent IS threats and conducted joint operations through CENTCOM with the Syrian government. This most notably culminated in Syria’s admission to the US-led Coalition in November 2025.

- However, this engagement has also emerged as a radicalizing factor fueling IS activity. For example, IS has criticized President al-Sharaa for abandoning his jihadist roots with HTS and cooperating with Western governments, which IS characterizes as “infidels.” This has included explicit criticism following the Premier’s meeting with US President Donald Trump in November 2025. Additionally, IS has used this as a recruitment tool to bolster its ranks, as underscored by its call for HTS members to defect following Syria’s admission to the International Coalition to Defeat IS, and more recently to foreign fighters, including Uzbeki groups, who have clashed with the government.

- The success of this strategy was demonstrated by a shooting attack that killed three American citizens during a joint patrol with government forces, which was perpetrated by an IS-linked member of Syria’s state security forces in December 2025. IS did not formally claim the attack, but referred to it as a “blow” against American and Syrian interests. This may suggest an increased emphasis on radicalization and the promotion of lone-wolf attacks, which could complicate detection efforts.

Iran-linked actors

- Iran-linked actors have emerged as another major threat in Syria. This is derived from their entrenched presence in the country, which constituted a major outpost of Iranian influence and support under Bashar al-Assad. President al-Sharaa has since renounced Iran’s role in Syria, with the new authorities implicating Hezbollah-linked actors in multiple attack plots in recent months. This has included the arrest of a terrorist cell suspected of launching Hezbollah-linked projectiles toward Damascus’ Mezzeh area between November 2025 and January 3, with authorities uncovering a heavily armed Hezbollah cell near the capital in September 2025.

- More recently, Syrian authorities arrested a suspected Hezbollah-affiliated cell in rural Damascus after a member planted an IED outside the residence of a religious figure near the Mariamite Cathedral in Damascus’ Bab Touma area on April 11. Taken together, these incidents underscore continued attempts by the Iran-led Axis of Resistance to undermine the new Western-aligned government, likely by capitalizing upon long-standing networks within Syria and the ability to smuggle local Syrian recruits across the porous border to Lebanon for training purposes.

- In this context, Iran-backed groups have also exploited security gaps in southern Syria to advance Tehran’s aims vis-a-vis Israel. This is reflected in Israel’s assessment that Iran-backed actors are present in Syrian locales near the Israeli border, triggering Israel’s decision to expand the buffer zone along the Golan Heights and launch localized raids in Syrian towns such as Beit Jinn. In turn, this will also sustain the risk of Israeli strikes and ground operations near the border.

Outlook:

FORECAST: The multi-faceted terrorist threat in Syria will remain one of the most prominent challenges facing the new government. Threat actors will seek to exploit vulnerabilities in the nascent security apparatus, which will require extensive support from international partners in the long term to curb the resurgence of IS and activity by Iran-linked groups. It will necessitate continued and intensified counter-militancy activity, which is expected to persist in the long term in Syria, and could lead to armed clashes given the proliferation of weapons among these groups. The risk of terror attacks within Syria will remain extreme, including in the capital and newly acquired territory near strategic infrastructure in northeastern Syria.

Sectarian Tensions

- Since the predominantly Sunni government took power following the Islamist HTS-led takeover, sectarian clashes have emerged as a major domestic and international concern. This is primarily due to the inclusion of armed factions, many of whom subscribe to extremist jihadist ideology, within the government’s security forces.

- In turn, this has prompted concerns over the authorities’ ability to control such elements, who may be liable to act autonomously against minority sects whom they view as “infidels.” This is compounded by resentment among segments of the Sunni populace following decades of Alawite rule under the al-Assad family, fueling their motivation to act extrajudicially.

- According to open-source data, the provinces of Latakia, as-Suweida, Tartus, Hama, and Homs, which all experienced outbreaks of sectarian violence involving Alawite and Druze communities, accounted for over 60 percent of political violence-related fatalities recorded nationwide in 2025. The Alawite-majority Tartus province recorded a 500 percent increase in political violence in 2025 compared to 2024, while the Druze province of as-Suweida saw a 200 percent year-on-year increase over the same period. This aligns with the most major outbreaks of sectarian violence recorded since the takeover, including in northwestern Syria in March 2025 and in as-Suweida in July 2025. These statistics highlight a geographical variation in the probability and scope of this threat vector materializing, which is significantly higher in minority-concentrated areas of northwestern and southern Syria.

- The cycles of violence have remained sporadic, marked by intermittent periods of calm disrupted by renewed clashes. This pattern suggests that the underlying volatility can be catalyzed by localized triggers. They also carry secondary risks, such as the eruption of large-scale protests denouncing sectarian violence. For example, tens of thousands of Alawites mobilized following a bout of sectarian violence in northwestern Syria in November 2025. These protests, typically led by prominent spiritual figures, are often accompanied by calls for federalism and greater autonomy, posing a challenge to the government’s efforts to consolidate administrative control nationwide.

- Although President al-Sharaa has made efforts to project accountability by launching investigations into some of the most serious eruptions of violence, the government’s inability to prevent violence against minorities has entrenched mistrust. It has also sustained international concerns over its ability to govern effectively for all sects in Syria.

- This has been compounded by political developments. Ballots were not held in minority areas during the national elections in November 2025, such as al-Hasakah and as-Suweida, due to security reasons. Although authorities have recently held elections in al-Hasakah and Kobani since the takeover from the AANES, Kurdish concerns regarding political representation persist. Additionally, political appointments have been perceived as biased based on minimal minority representation in the first post-transition elections and the composition of the People’s Assembly. Collectively, these developments have reinforced perceptions of political and social exclusion among Kurdish, Alawite, and Druze communities, who remain wary of President al-Sharaa’s Islamist roots.

Outlook:

FORECAST: While calls for federalism are unlikely to materialize into autonomy, they are expected to fuel protests and localized unrest, with sectarian mistrust likely to remain a key driver of instability in Syria. This will pose significant credibility risks for President al-Sharaa and his government, which will prompt him to pursue inclusivity reforms. However, minority-dominated areas in northeastern, coastal, and southern Syria are expected to remain the primary high-risk hotspots for violence, which could erupt at short notice. This will create a risk to operations in areas with strategic assets, including the Tartus and Latakia Ports, where supply chains, infrastructure, and workforce stability could be threatened. The associated spillover risks of collateral damage may also impact insurance costs. In case of broader violence, the imposition of curfews and restricted zones is liable to delay projects and undermine investor confidence.

Conclusion:

The easing of sanctions throughout 2025, culminating in the repeal of the Caesar Act, substantially reduced the legal, regulatory, and compliance barriers that had effectively precluded international engagement with Syria for over a decade. This is expected to result in a gradual increase in commercial and financial activity in 2026, particularly as regional and Western actors deepen their economic and diplomatic engagement with Damascus. Nonetheless, despite the removal of these former legal restraints, extensive infrastructure damage, persistent energy shortages, uneven transport connectivity, and underdeveloped banking channels will continue to constrain the pace, scale, and viability of re-entry for prospective businesses. Additionally, despite a relative improvement in the security landscape since the takeover, Syria remains an extreme-risk country, with multiple threat vectors posing risks to personnel, assets, and the continuity of operations, particularly in northeastern, southern, and coastal regions.

Recommendations:

Travel:

- Avoid all travel to Syria due to the volatile security environment, including the elevated risks of militancy, armed conflict, and sectarian violence.

- Those conducting business-critical operations in Syria are advised to take security precautions, including:

- Prior to travel, conduct timely risk assessments and close monitoring of the situation on the ground.

- Implement physical security arrangements, including security escorts and a local fixer to facilitate coordination with Syrian government authorities.

- Use only vetted and secure private transportation from a hotel, company, or organization.

- Consult with us at [email protected] or +44 20-3540-0434 for custom risk assessments and contingency planning.

Security risks:

- Continue to avoid all travel to northeastern Syria given the continued risk of localized eruptions of armed conflict.

- Remain cognizant of the extreme risk posed by jihadist militant groups in the country, including the Islamic State (IS), and Iran-linked actors.

- Western nationals are advised to maintain a low profile throughout Syria in light of the elevated militant threat. Minimize exposure to large outdoor gatherings.

- Remain cognizant of the elevated risk of sectarian violence in the country, particularly in and around as-Suweida, Latakia and Tartus provinces, and Kurdish-dominated parts of northeastern Syria.

- Avoid travel to these areas given the elevated risk of sectarian violence, and avoid discussing sectarian issues in public due to heightened sensitivities.

Structural risks:

- Businesses are advised to commission professional legal reviews prior to entering the Syrian market to ensure compliance with regulations in the country.

- Considering the heightened risk of unpredictable power outages, take mitigatory measures, such as confirming that business locations have working generators and sufficient access to fuel for longer periods.

Authors:

This report was written by:

- Ishika Garg – Intelligence Manager, MENA Division

- Matteo Sbarigia – Intelligence Manager, MENA Division

And reviewed by:

- Kez Gould – Associate Director, MENA Division

Executive Summary:

- International sanctions relief throughout 2025, culminating in the repeal of the Caesar Act, underscored Western confidence in the new Syrian government and substantially reduced the legal and compliance barriers that had precluded international engagement with the country.

- This is expected to enable a gradual increase in investment and commercial activity, although multiple structural and security risks will continue to challenge a return to operations in Syria.

- Extensive infrastructure damage, persistent electricity shortages, and underdeveloped banking channels will contribute to elevated logistics and operating costs, constraining the pace and scale of foreign companies’ re-entry.

- Despite a relative stabilization of the security environment, the risk of armed conflict, militancy, and sectarian violence will compound threats to personnel and assets.

- Overall, this will necessitate adherence to safety precautions and extensive contingency planning to initiate and sustain operations, despite the emerging range of business opportunities in the country.

Introduction:

Since the ousting of Bashar al-Assad in December 2024, the President Ahmad al-Sharaa-led government has rapidly reconfigured its foreign relations, governance structures, and economic orientation. Early outreach by Turkey and Qatar, including the reopening of diplomatic missions and the provision of energy and logistical support, was followed by participation from major regional powers, including Saudi Arabia and the UAE. Western governments adopted a more cautious approach, initially conditioning deeper engagement on security cooperation, protection of minorities, and a demonstrable shift from the former government’s authoritarianism toward inclusive governance. Despite some setbacks, President al-Sharaa formed a transitional government and reached several major milestones. This included integrating many non-armed groups into the Ministry of Defense and holding parliamentary elections in October 2025. These measures have been deemed sufficient by the West to create conditions for expanded international involvement in Syria after more than a decade of isolation. This has resulted in notable, high-level diplomatic engagement, including Syrian state visits to Washington, delegations of foreign officials visiting Damascus, and the easing of the wide-ranging, crippling sanctions regime imposed on Syria under al-Assad.

Assessments & Forecast:

Repeal of Caesar Act marks milestone in sanctions relief

- The gradual dismantling of the extensive sanctions architecture throughout 2025, including the issuance of temporary waivers by the US and the removal of punitive measures against certain sectors, culminated in the milestone repeal of the 2019 Caesar Syria Civilian Protection Act (Caesar Act) in December 2025.

- The Caesar Act sanctions were among the most stringent measures imposed on Syria under al-Assad. The provisions extended secondary sanctions to non-US actors who engaged in construction, energy, and financial dealings with Syrian state entities. This became the primary deterrent constraining international engagement or investment in Syria, with its secondary-sanctions design carrying significant legal and reputational exposure risks, triggering a risk-averse approach among foreign firms even where activity was technically permissible.

- Decisions taken by President Trump’s administration throughout 2025 reflect its assessment that the sanctions in place at that time would significantly constrain the new government’s ability to initiate Syria’s socioeconomic recovery. This is underscored by the decision to issue General License (GL) 25 in May 2025, which marked another milestone providing immediate sanctions relief for a broad range of activities.

- Similarly, the US Treasury’s Office of Foreign Assets Control (OFAC) removed the Syrian Sanctions Regulations and delisted most Syrian entities after an Executive Order (EO) signed in June 2025, effectively terminating the old Syria sanctions program. This, along with the US Department of Commerce’s easing of export licensing requirements for civilian goods and software in August 2025, provided the most significant legal basis for updating corporate compliance frameworks and facilitated the re-entry of civilian technology and service providers into the Syrian market. This was evidenced by the return of several multinational technology company operations, including Google, Apple, Samsung, and Meta, between August and October 2025.

- The permanent repeal of the Caesar Act was, however, the most consequential step because it removed the remaining source of uncertainty surrounding the durability of sanctions relief up until this point. While the Trump administration’s 180-day waivers in May and November 2025 had already eased restrictions in practice, the temporary nature of these measures sustained investor caution driven by the short renewal cycle and the persistent risk of reversals, which are of particular importance for longer-term contracts and engagement.

- In addition to the permanent nature of the move, the legislative repeal in the National Defense Authorization Act for Fiscal Year 2026 eliminated the legal basis for the automatic reimposition of sanctions after each waiver expired. This was replaced with a review mechanism focused on periodic White House reports to Congress on the Syrian government’s counter-Islamic State (IS) efforts, protection of minorities, and the role of foreign fighters within state institutions. In turn, this now renders sanctions enforcement solely subject to political oversight, diluting mandatory compliance requirements for the Syrian government to non-binding commitments it should aspire to meet.

- FORECAST: A broad reimposition of sanctions on Syria is therefore highly unlikely, although targeted restrictions on specific individuals and entities remain in place. Gulf countries also actively advocated for sanctions relief, entrenching their political and financial interests in Syria’s recovery efforts. This will provide an additional layer of stakeholders interested in preventing a renewed economic isolation of Syria by the West.

- FORECAST: Overall, this will reduce the compliance risks associated with operating in Syria, which will likely prompt an increase in entities seeking to re-enter the country for business in 2026. This report will examine the continued logistical challenges and security risks associated with operating in Syria.

Infrastructural challenges:

- Infrastructure in Syria has been severely degraded by over a decade of civil war and sanctions-driven restrictions on recovery. The World Bank has estimated total damage to physical, social, and other infrastructure at approximately 8.7-11.3 billion USD. Transport networks, electricity generation and distribution, and water and sanitation systems were among the most heavily affected sectors, pointing to the scale of damaged infrastructure that the new authorities must rehabilitate.

- In this context, Syrian authorities have increasingly sought to formalize reconstruction opportunities for private investors. This is evidenced by the Syrian Investment Authority’s (SIA) publication of hundreds of projects across the infrastructure, logistics, tourism, and services sectors.

- Many are structured as Build-Own-Operate (BOO), Build-Transfer-Operate (BTO), or broader Public-Private Partnership (PPP)-style arrangements, reflecting Damascus’ efforts to attract foreign private capital. This is likely due to the state’s limited fiscal capacity and the scale of reconstruction needs. However, the viability and timelines of such projects will continue to be hindered by implementation challenges, including infrastructure-related issues discussed below, which will pose a significant hurdle for businesses looking to enter Syria.

Transportation

Air travel

- Since the Hay’at Tahrir al-Sham (HTS)-led takeover, international connectivity has improved more rapidly than domestic networks. Damascus International Airport (DAM) reopened to international traffic in January 2025, followed by Aleppo International Airport (ALP) in March 2025, underscoring the prioritization of Syrian authorities to restore international access and logistical connectivity, which will likely be critical for Syria’s broader socioeconomic recovery.

- However, passenger and cargo flow reportedly continues to rely heavily on outdated digital infrastructure, including in air traffic control centers. Airports also reportedly lack appropriate radar equipment, while significant concerns persist over the authorities’ ability to meet international aviation standards. The need to upgrade Syria’s airport infrastructure is pertinently demonstrated by major deals signed in recent months to modernize state facilities. This includes a four billion USD deal to upgrade DAM signed in November 2025 with a Qatar-led consortium, in addition to a major deal signed with Saudi Arabia on February 7 entailing the establishment of a joint Syrian airline, the redevelopment of ALP, and the construction of a new airport in Aleppo.

- FORECAST: While these major strategic projects will significantly improve Syria’s international connectivity in the long term, short-term challenges will persist, hindering the country’s ability to absorb a considerable uptick in air traffic. This will continue to impact businesses on the ground in 2026, particularly for time-sensitive logistics.

Land travel

- Overland connectivity has slowly improved since December 2024. This has been partly facilitated by Syria’s reintegration into regional transport networks, as evidenced by the June 2025 MoU between Ankara and Damascus abolishing transshipment requirements at border crossings. While such deals will ease administrative constraints on direct road transport and freight movement on key corridors linking Syria with Turkey, Jordan, and the Gulf, considerable challenges will remain to domestic road travel.

- Degraded road conditions and inconsistent maintenance will keep transit times and accident risks elevated, particularly for movements on more minor roads and outside major urban centers. Prominent thoroughfares will also require extensive rehabilitation. This includes the M4 highway, connecting Aleppo to Raqqa and the northeast, which was impacted by the territorial fragmentation between the Syrian Democratic Forces (SDF) and the central government, preventing restoration work along a logistics corridor.

- Travel within Syria will be further constrained by the continued paralysis of large segments of Syria’s rail network. The Syrian Transport Minister reportedly stated that only 1,052km of rail networks are functioning out of 2,800km available, with repairs estimated to cost around 5.5 billion USD, which would take between three and five years to complete.

- FORECAST: This will further constrain logistics for businesses seeking to operate in the country, which may impede the internal transfer of materials, particularly in the construction sector. However, significant investments are likely in the long term, with reported tripartite discussions to establish a transnational railway from Turkey to Saudi Arabia through Syria and Jordan.

Sea travel

- Maritime connectivity demonstrated clear signs of recovery in 2025. A maritime data company reported a 769 percent surge in seaborne trade in December 2025 compared to December 2024. This underscores that Syria’s ports of Tartus, Latakia, and Baniyas are already capable of supporting basic commercial operations and accommodating higher vessel arrivals and cargo volumes.

- This trend is likely to accelerate in 2026, with foreign firms expected to explore investments in Syria’s maritime infrastructure given its strategic location on the Mediterranean Sea. This is already demonstrated by major deals signed last year, including the May 2025 agreements with France’s CMA CGM for the Latakia Port and the UAE’s DP World for the Tartus Port, highlighting the willingness of foreign operators to pursue long-term deals in Syria within the emerging post-sanctions framework.

- FORECAST: That said, such agreements and projects will take several years to implement and complete. Outdated handling equipment, limited channel depth for larger vessels, and the absence of fully integrated port systems will continue to limit port capacity and efficiency in the short term at least. Syria’s ports will therefore likely remain vulnerable to handling surges in demand, adverse weather conditions, and potential congestion, which could mean prolonged vessel waiting times, unreliability of schedules, supply chain disruptions, and higher logistics costs.

Energy

- Energy availability remains one of the most immediate constraints on economic stabilization and the re-entry of businesses in the country due to Syria’s degraded generation capacity and transmission infrastructure through many years of civil war and fragmented territorial control.

- Prior to the civil war, Syria was estimated to have around 8,500 MW of installed power capacity. However, in February 2025, the Energy Ministry indicated that this had fallen to 1,300 MW, likely due to damage to power plants, transmission lines, and distribution networks, and a lack of fuel preventing plants from operating at full capacity.

- Despite some improvements over the past year, particularly in major cities such as Damascus, where electricity coverage appears to have steadily increased, challenges will likely remain. Syria is estimated to require approximately 6,500 MW to provide 24-hour electricity coverage. This will require years of sustained investment and major repairs to the grid.

- Another critical factor will be re-establishing a reliable fuel supply. Several agreements with foreign countries over the past year underscore that Syria is not self-sufficient in this regard. This is despite extensive oil and gas reserves that are primarily located in the northeastern region, which formerly fell under Kurdish, rather than government, control. In this context, energy flows from this area were previously subjected to disruptions due to the state of armed conflict in recent years. This is both in terms of physical distribution, which was impeded by damaged infrastructure, and the lack of cooperation between the state and Kurdish forces overseeing output and distribution from this region.

- However, the January 30 comprehensive agreement between the Syrian government and the SDF formalized the integration of territory and energy resources previously held by the Kurdish forces under state control. This will enable the resumption of crude oil and gas transfers toward refineries in western Syria, improving fuel supply and energy generation. It will complement energy supply agreements signed with foreign partners over the last year. These included a March 2025 arrangement to supply LNG from Qatar via Jordan to the Deir Ali plant, south of Damascus, and the supply of Azerbaijani gas via Turkey to Aleppo through Qatari funding since August 2025.

- Additionally, major energy disruptions resulting from the US/Israel and Iran war have elevated Syria’s strategic relevance as an energy and transit corridor. On April 16, Iraq announced the commencement of crude loading operations through Syria’s Baniyas terminal for export to European markets under a transit-and-re-export arrangement, with Syria retaining a portion of the crude to support domestic power generation. This was followed by Iraq’s May 1 announcement that oil exports to Syria through the recently reopened Rabia border crossing had formally resumed. These developments underscore Syria’s strategic geographical positioning linking Iraq, the Gulf, and the Mediterranean Sea, which Damascus will continue to leverage to attract foreign investment in the sector. This is particularly amid ongoing uncertainty over the viability of oil and gas exports via the Persian Gulf, which partly undermines enthusiasm for the India-Middle East-Europe Economic Corridor (IMEC), which was a key scheme promoted by Washington during former President Joe Biden’s term.

- FORECAST: In 2026, energy availability is therefore expected to improve incrementally, particularly in urban and industrial zones. However, electricity shortages resulting in regular and potentially widespread outages will persist in the coming months, particularly in outlying areas outside major cities. This will constrain operations, logistics, and energy-intensive activities, with companies required to utilize private generators and integrate unplanned outages into their costs.

Banking and financial sectors

- Another major consideration for businesses looking to re-enter Syria for operations in 2026 will be the financial landscape. Banking, insurance, and trade finance adjusted more slowly to the gradual lifting of sanctions in 2025. The reconnection of international payment networks, namely Visa and Mastercard, to Syrian domestic banks on May 4 already constitutes a critical step toward facilitating e-commerce, reducing reliance on cash transactions and informal channels, and gradually improving payment processing capabilities for businesses operating in Syria.

- However, correspondent banking relationships (CBRs) and cross-border financial channels, which had been previously severed, only began to be re-established in 2025. This was supported by the easing of restrictions on Syrian financial institutions by Western countries in 2025 and 2026, including measures permitting correspondent engagement with the Commercial Bank of Syria. However, the slow progress has constrained access to trade finance, letters of credit, and cross-border settlement, reflecting the cumulative effect of prior compliance with sanctions and heightened Anti-Money Laundering and Counter-Terrorism Financing (AML/CFT) requirements. Syria’s continued grey-listing by the Financial Action Task Force (FATF) compounded this by increasing due diligence requirements and scrutiny by international banks, even in the absence of explicit prohibitions.

- The Central Bank of Syria’s (CBS) reconnection to the SWIFT international payments system in November 2025 marked a milestone, restoring Syria’s ability to process trade-related payments, route remittances through formal channels, and improve transparency for international trade and foreign investment. However, its impact remains contingent on partner banks’ likely limited willingness to establish or expand CBRs. This is particularly given that Syria continues to be designated as a State Sponsor of Terrorism (SST) by the US State Department, sustaining elevated reputational risks. This will continue to discourage large Western banks, insurers, and investors from funding projects or backing businesses operating in Syria.

- FORECAST: Overall, this highlights that firms and businesses seeking to engage in Syria in 2026 will continue to face challenges, despite increasing access to banking and financing in the country. Financial flows will likely require routing through a limited number of regional banks, which, together with the substantial difficulties in establishing CBRs, will increase processing times and transaction costs. While the SST designation, based on the trajectory of US actions in 2025, is likely to be rescinded in the coming months, it will continue to constrain access to credit in the short term at least. Combined, these factors will elevate costs for businesses.

Security challenges:

In addition to economic hurdles, there are a range of security issues that will challenge business re-entry into Syria. While the overall security environment has stabilized, it remains fragmented and volatile in different areas. The key drivers of instability include the risk of armed conflict, militancy, and sectarian tensions.

Armed Conflict

Since the December 2024 takeover, the government has focused on the integration and gradual monopolization of armed groups and territorial control in Syria. Despite relatively broad success in both endeavors, including the integration of most non-state actors into the Ministry of Defense in January 2025 and the establishment of government control across most territory, several outlying challenges persist. These unresolved issues continue to generate localized clashes, which at times escalate into broader waves of armed confrontations.

Kurdish forces in northeastern Syria

- Despite the March 2025 agreement for the Kurdish Syrian Democratic Forces (SDF) and Autonomous Administration of North and East Syria (AANES) to integrate into state structures, this process became stagnated and resulted in eruptions of largely localized armed clashes throughout the year in northeastern Syria. This was primarily due to Kurdish resistance to integrate over concerns regarding the conduct of the Islamist government forces against the Kurdish population and its desire to retain some autonomy.

- The failure to implement the framework resulted in a major eruption of armed conflict in January, following the government’s decision to launch rapid offensives to oust Kurdish forces in Aleppo city, the wider province, and eventually vast swathes of northeastern Syria that were under AANES control. The success of the government campaign, which significantly increased Damascus’ leverage, in addition to pressure from international stakeholders such as Turkey and the US, prompted the SDF and AANES to sign a comprehensive ceasefire deal on January 30.

- Under the framework, the government has begun to assume control of all territory, integrate former SDF brigades into the Syrian Arab Army (SAA), and grant Kurdish military figures largely symbolic positions. No major flare-ups of hostilities have materialized since, constituting a success for Damascus and leading to relative stabilization in the region.

- FORECAST: However, mistrust persists between the Islamist government and segments of the Kurdish forces/population, resulting in localized and sporadic instances of unrest during the government’s takeover in some areas. This risk will persist, with more likely hotspots being the Kurdish-majority cities of Kobani and Qamishli, where government forces will be deployed, and in the mixed al-Hasakah city, which was a major point of contention in the latest campaign.

- FORECAST: Moreover, despite initial success in the integration of some SDF units into the SAA and the deployment of these forces to potential friction points formerly held by the AANES, practical gaps remain. This includes the alignment and training of forces. Additionally, former SDF Commander and now Deputy Defense Minister of the Eastern Region Siban Hamo warned that the number of former SDF personnel exceeds the new brigades that have been formed. This increases the risk of disenfranchisement, which could lead sidelined former SDF fighters to join more hardline groups that refused to integrate with the SAA. Such militias could resort to attacking government positions.

- Concurrently, Damascus will face the challenge of controlling more radical armed factions that were integrated into its ranks shortly after the ousting of al-Assad, several of whom were suspected of perpetrating atrocities during previous bouts of sectarian clashes over the last year (see below). Such actors could also oppose the integration of former SDF personnel into the national military.

- FORECAST: Overall, this will sustain volatility in the region. This is an important consideration for both potential investors in Syria and the government, given the high concentration of strategic infrastructure in northeastern Syria, including energy assets, transportation hubs, and logistics infrastructure (see infographic below).

Druze forces in southern Syria’s as-Suweida

- Another major arena for armed conflict is southern Syria’s Druze-majority as-Suweida, which continues to be governed by Druze religious leadership. This includes Hikmat al-Hijri, who established the National Guard and strongly opposes the influence of the Islamist government, with which it has clashed on several occasions since December 2024.

- The most notable eruption occurred in July 2025, triggered by mutual kidnappings by Bedouin residents near as-Suweida and Druze militiamen. This prompted extensive violence, including clashes on major thoroughfares in the area such as Route 110, which also spread to Druze locales near Damascus such as Rif Dimashq’s Jaramana and Sahnaya.

- As underscored in this outbreak, sectarian violence specifically involving Syria’s Druze community is also a trigger for Israeli strikes, reflecting Jerusalem’s pledge to protect the sect from perceived extremists within the government. This has entailed Israeli warning strikes against the Syrian government’s military infrastructure in Damascus, in addition to periodic strikes against such assets in southern Syria.

- FORECAST: Following the government’s offensive against Kurdish forces in northeastern Syria, tensions and the Druze threat perception toward Damascus have likely increased. This is supported by al-Hijri’s calls for protests and a large-scale demonstration recorded in as-Suweida demanding Druze self-determination on January 31, in addition to sustained, localized clashes recorded since.

- FORECAST: This may suggest that some of the Druze leadership view the Syrian government’s offensive against Kurdish forces as preluding a similar operation against the Druze in as-Suweida. This is particularly given the organized opposition in the province, including politically through the “Supreme Legal Committee,” and militarily through the National Guard, which are both under the influence of Hikmat al-Hijri, who enjoys popular support. In this vein, the government likely views the Druze community as capable of offering more cohesive and sustained resistance to government forces and thus posing a threat to the government.

- FORECAST: While any potential plans for a broader government operation were likely delayed amid the regional war and evolving security priorities, the risk for such a scenario will be elevated over the coming months. As the final major area falling outside government control, as-Suweida will likely remain a sensitive and potentially volatile arena, with any renewed escalation carrying risks of collateral damage and operational disruptions.

al-Assad loyalists in northwestern Syria

- While relatively less organized than Druze and Kurdish militias, cells affiliated with former President Bashar al-Assad also pose a threat to the new government and undergird the risk of armed conflict in the country. These elements are primarily concentrated in former al-Assad strongholds, particularly in northwestern Alawite coastal areas such as the Latakia and Tartus provinces, where sporadic attacks have been recorded. For example, following the HTS-led takeover, al-Assad loyalists launched a series of attacks against government forces in January 2025, followed by a coordinated attack in the Jableh area in March 2025.

- Loyalist groups, such as the Coastal Shield Brigade, the Men of Light Brigade, and the Syrian Popular Resistance, appear largely fragmented. They likely comprise security personnel of the former regime, local militia members, and tribal networks with historical ties to the al-Assad establishment. There is no clear unified command structure or identifiable umbrella organization directing or coordinating operations. As a result, attacks by al-Assad loyalists have not followed a fixed pattern and have occurred sporadically. This trend is likely to continue.

- FORECAST: In the absence of a more organized and cohesive loyalist network, these actors are unlikely to pose a significant challenge to the authorities in terms of contesting territorial control. However, they are likely to continue launching asymmetric attacks to undermine the government. An uptick in attacks may trigger targeted security operations against localized cells, which could lead to armed clashes or surges of retaliatory violence that would increase the risk of collateral damage. This risk of cyclical violence will likely be elevated around events of national significance, such as Liberation Day, marking the overthrow of al-Assad’s government.

Outlook:

FORECAST: Overall, these threat vectors depict several higher-risk areas of the country for armed conflict: Kurdish-majority parts of northeastern Syria, southern Syria’s Druze-majority as-Suweida, and Alawite regions in the northwestern part of the country. This will continue to pose a major challenge given the significant threat of collateral damage to employees and assets, which will increase both risks and insurance costs, in addition to disruptions to operations associated with outbreaks of violence. These threats are expected to persist in the coming year as the government continues to consolidate its control over territory and outstanding armed groups.

Militancy

Militancy poses one of the most significant security risks to the government and business operations in the country. Since December 2024, Syria has witnessed several high-profile terrorist attacks (see infographic below). These have ranged from targeted attacks against minority institutions, state facilities, government forces, and on one occasion against US forces. The primary actors perpetuating this threat are jihadist groups and Iran-linked actors.

Jihadist actors

- Despite its broad decline in recent years, the security vacuum that emerged following al-Assad’s ousting and the presence of large, abandoned SAA weapons depots and warehouses enabled the Islamic State (IS) to access military-grade weapons. This has bolstered its operational capabilities, boosted the group’s morale, and led to an apparent uptick in IS attacks and concerns of a resurgence in the country.

- According to open-source data, the top three provinces affected by IS attacks are Deir Ezzor, al-Hasakah, and Raqqa (see heat map below), highlighting the significant terror threat in northeastern Syria, where many strategic assets such as oil and gas fields are located. This may be due to security gaps arising along former frontlines of territorial control between the government and AANES, particularly in Deir Ezzor and al-Hasakah, as underscored by recent IS-claimed attacks in these locales. Several such incidents have taken place near strategic transport routes, including the M5 highway, highlighting IS’s ability to threaten critical infrastructure and disrupt business operations across Syria.

- Areas surrounding Damascus in Rif Dimashq province have emerged as another particularly notable flashpoint for such activity, as similarly depicted in the heatmap and the infographic below. Successful jihadist attacks, either by IS or the affiliated Saraya al-Sunnah, have also materialized in the capital, including a suicide bombing at the Mar Elias Church perpetrated by Saraya al-Sunnah in June 2025, and an IS-claimed IED attack targeting a Shiite cleric in Sayeda Zainab, located between DAM and Damascus, on May 1.

- Additionally, this region has recorded one of the highest numbers of counter-militancy operations (eight) since Syria’s admission to the US-led Coalition to Defeat IS in November 2025. Authorities have seized military-grade arms and high-ranking IS members in outlying areas near the capital, pointing to a significant threat of militancy near Damascus, which likely remains a key target for the group. This is particularly in light of the anticipated influx of business operations, which are likely to have some presence in the capital or at least pass through it, given its status as a major transport hub in the country.

- The gravity of the IS threat is further underscored by the extent to which Western engagement with Syria has focused on countering the group’s resurgence. This has become a focal point of cooperation, with the US, UK, and France conducting airstrikes on IS sites in recent months, while Washington has also shared intelligence of imminent IS threats and conducted joint operations through CENTCOM with the Syrian government. This most notably culminated in Syria’s admission to the US-led Coalition in November 2025.

- However, this engagement has also emerged as a radicalizing factor fueling IS activity. For example, IS has criticized President al-Sharaa for abandoning his jihadist roots with HTS and cooperating with Western governments, which IS characterizes as “infidels.” This has included explicit criticism following the Premier’s meeting with US President Donald Trump in November 2025. Additionally, IS has used this as a recruitment tool to bolster its ranks, as underscored by its call for HTS members to defect following Syria’s admission to the International Coalition to Defeat IS, and more recently to foreign fighters, including Uzbeki groups, who have clashed with the government.

- The success of this strategy was demonstrated by a shooting attack that killed three American citizens during a joint patrol with government forces, which was perpetrated by an IS-linked member of Syria’s state security forces in December 2025. IS did not formally claim the attack, but referred to it as a “blow” against American and Syrian interests. This may suggest an increased emphasis on radicalization and the promotion of lone-wolf attacks, which could complicate detection efforts.

Iran-linked actors

- Iran-linked actors have emerged as another major threat in Syria. This is derived from their entrenched presence in the country, which constituted a major outpost of Iranian influence and support under Bashar al-Assad. President al-Sharaa has since renounced Iran’s role in Syria, with the new authorities implicating Hezbollah-linked actors in multiple attack plots in recent months. This has included the arrest of a terrorist cell suspected of launching Hezbollah-linked projectiles toward Damascus’ Mezzeh area between November 2025 and January 3, with authorities uncovering a heavily armed Hezbollah cell near the capital in September 2025.

- More recently, Syrian authorities arrested a suspected Hezbollah-affiliated cell in rural Damascus after a member planted an IED outside the residence of a religious figure near the Mariamite Cathedral in Damascus’ Bab Touma area on April 11. Taken together, these incidents underscore continued attempts by the Iran-led Axis of Resistance to undermine the new Western-aligned government, likely by capitalizing upon long-standing networks within Syria and the ability to smuggle local Syrian recruits across the porous border to Lebanon for training purposes.